The Importance of a Budget: Knowing Where Your Money Goes

Many people believe that managing money is only about knowing how much you earn. While income is important, it is only half of the picture. What truly determines financial success is understanding where your money goes. A budget is the tool that makes this possible. It helps you control your spending, prepare for the future, and create savings that can later be used for investing.

What Is a Budget?

A budget is a plan for your money. It shows how much money comes in and how much goes out over a certain period of time, usually a month. Instead of guessing or hoping there will be money left at the end, a budget gives every dollar a purpose.

Without a budget, money often disappears on small, unplanned expenses. These may seem harmless at first, but over time they can prevent you from saving or reaching financial goals.

Why Knowing Where Your Money Goes Matters More Than Income

Many people earn a decent amount of money but still struggle financially. This usually happens because they do not track their spending. Knowing your income tells you what is possible, but knowing your expenses tells you what is real.

When you track where your money goes, you can:

-

Identify unnecessary or impulsive spending

-

See patterns in your habits

-

Make better decisions about priorities

-

Avoid debt caused by overspending

Small daily expenses—such as snacks, subscriptions, or transport costs—add up quickly. A budget reveals these hidden costs and gives you the chance to change them.

The Benefits of Budgeting

Budgeting provides both short-term and long-term benefits:

-

Financial control: You decide how money is used instead of reacting when it is gone.

-

Reduced stress: Knowing your bills and savings are covered brings peace of mind.

-

Goal setting: A budget helps you save for education, emergencies, or future investments.

-

Discipline: It encourages responsible spending and delayed gratification.

Most importantly, budgeting creates the foundation for saving and investing.

How to Create a Simple Budget

Creating a budget does not have to be complicated. The key is honesty and consistency.

-

List your income

Write down all sources of income, such as allowances, part-time work, or gifts. -

Track your expenses

Divide expenses into fixed (rent, school fees, transport) and variable (food, entertainment, shopping). -

Compare income and expenses

This shows whether you are living within your means or spending more than you earn. -

Set limits

Decide how much you can spend in each category and stick to it. -

Review regularly

A budget should be checked and adjusted as your income or goals change.

Creating Savings Through Budgeting

Savings do not happen by accident—they are planned. A good budget treats savings as a priority, not as leftover money.

One effective approach is to pay yourself first. This means setting aside a portion of your income for savings before spending on anything else. Even a small amount saved consistently can grow over time.

Tips for building savings:

-

Start small and increase gradually

-

Separate savings from spending money

-

Avoid unnecessary purchases

-

Set clear savings goals

Savings act as a safety net for emergencies and prevent the need for borrowing.

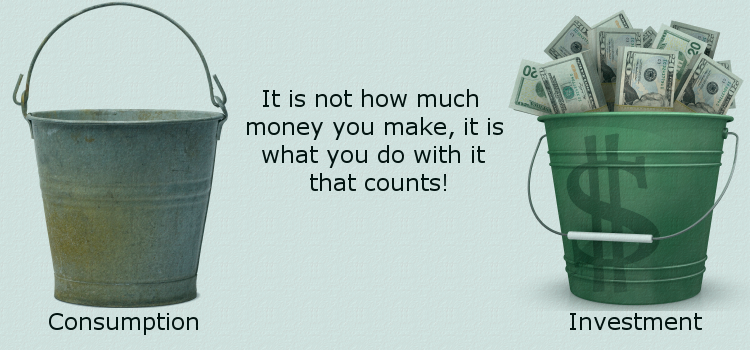

From Saving to Investing

Once you have built consistent savings, you can begin thinking about investing. Investing allows your money to grow by earning returns over time. However, investing without savings is risky. Savings provide security, while investing builds wealth.

A budget makes investing possible by:

-

Creating surplus money

-

Encouraging long-term thinking

-

Teaching discipline and patience

Before investing, it is important to understand the risks and start with safe, age-appropriate options under proper guidance.

Conclusion

A budget is more than a financial document—it is a life skill. While knowing how much money comes in is important, knowing where it goes is even more powerful. Budgeting helps you take control of your finances, build savings, and prepare for investing. By developing good budgeting habits early, you set yourself up for financial independence and long-term success.

Sample Monthly Budget Chart

Below is a simple example of a monthly budget for a student or young person with a small income.

Monthly Income

| Source of Income | Amount |

|---|---|

| Allowance / Part-time job | $300 |

| Total Income | $300 |

Monthly Expenses and Savings

| Category | Amount | Percentage of Income |

|---|---|---|

| Transportation | $60 | 20% |

| Food & Snacks | $70 | 23% |

| Phone/Data | $30 | 10% |

| Entertainment | $40 | 13% |

| School Supplies | $20 | 7% |

| Savings | $80 | 27% |

| Total | $300 | 100% |

This chart clearly shows where the money is going, not just how much is coming in.

Visual Budget Breakdown (Pie-Style Explanation)

If this budget were shown as a pie chart, it would look like this conceptually:

-

Savings – 27%

Savings – 27% -

Transportation – 20%

Transportation – 20% -

Food – 23%

Food – 23% -

Entertainment – 13%

Entertainment – 13% -

Phone/Data – 10%

Phone/Data – 10% -

School Supplies – 7%

School Supplies – 7%

This visual breakdown makes it easy to see whether spending aligns with priorities. The largest portion going to savings is a positive sign of good money management.

How This Budget Creates Savings for Investing

In this example, $80 is saved every month. Over time, savings grow:

| Time Period | Total Saved |

|---|---|

| 3 months | $240 |

| 6 months | $480 |

| 12 months | $960 |

Once savings become consistent, part of this money can be set aside for investing, while some remains for emergencies.

For example:

-

$50 → Emergency savings

-

$30 → Future investing fund

This approach reduces risk and builds financial confidence.

Simple Budget Rule

A common beginner rule is the 50–30–20 rule:

-

50% for needs

-

30% for wants

-

20% for savings

Even if the percentages change, the key idea remains the same: saving must be planned, not accidental.